You have an election to make at retirement, and you have three choices. Are you going to leave your spouse 50% of your annuity? If so, you will take a 10% reduction while you're living. The cost will be 10 percent. Alternatively, you can leave them 25 percent at a 5 percent cost, or leave them nothing. You have to choose one of these three options for your FERS retirement system: the 10 percent, the 5 percent, or no reduction in your pension for the rest of your life in exchange for a benefit when you die for your spouse. What do we call that class? When you die and somebody else gets a benefit, that's life insurance. You did it! That's right. So now you have your biggest life insurance decision ever made still in front of you. That was not what you thought coming in today, was it? We're talking 10% of your annuity for the rest of your days. So, let's walk through an example of retiring. You have a $22,000 annuity. 10% of that is $2,200 a year, right? That means you're drawing $20,000 a year. If you pass away, your spouse gets $11,000, which is 50% of the larger $22,000 number. Okay, there it is. There's your cost of insurance and the benefit that they get. Now, let's just assume by accident both of you live 25 years from that date, with colas being built into your pensions. Now, your gross pension would have been $36,000, but 10% of that is $3,600 a year, leaving you with $32,000 a year. If you die, your spouse gets $18,000. So, you have paid $72,000 over that 25-year period just in case you would have died. Your spouse would have picked up a monthly check. If your spouse...

Award-winning PDF software

Fers basic employee death benefit 2024 Form: What You Should Know

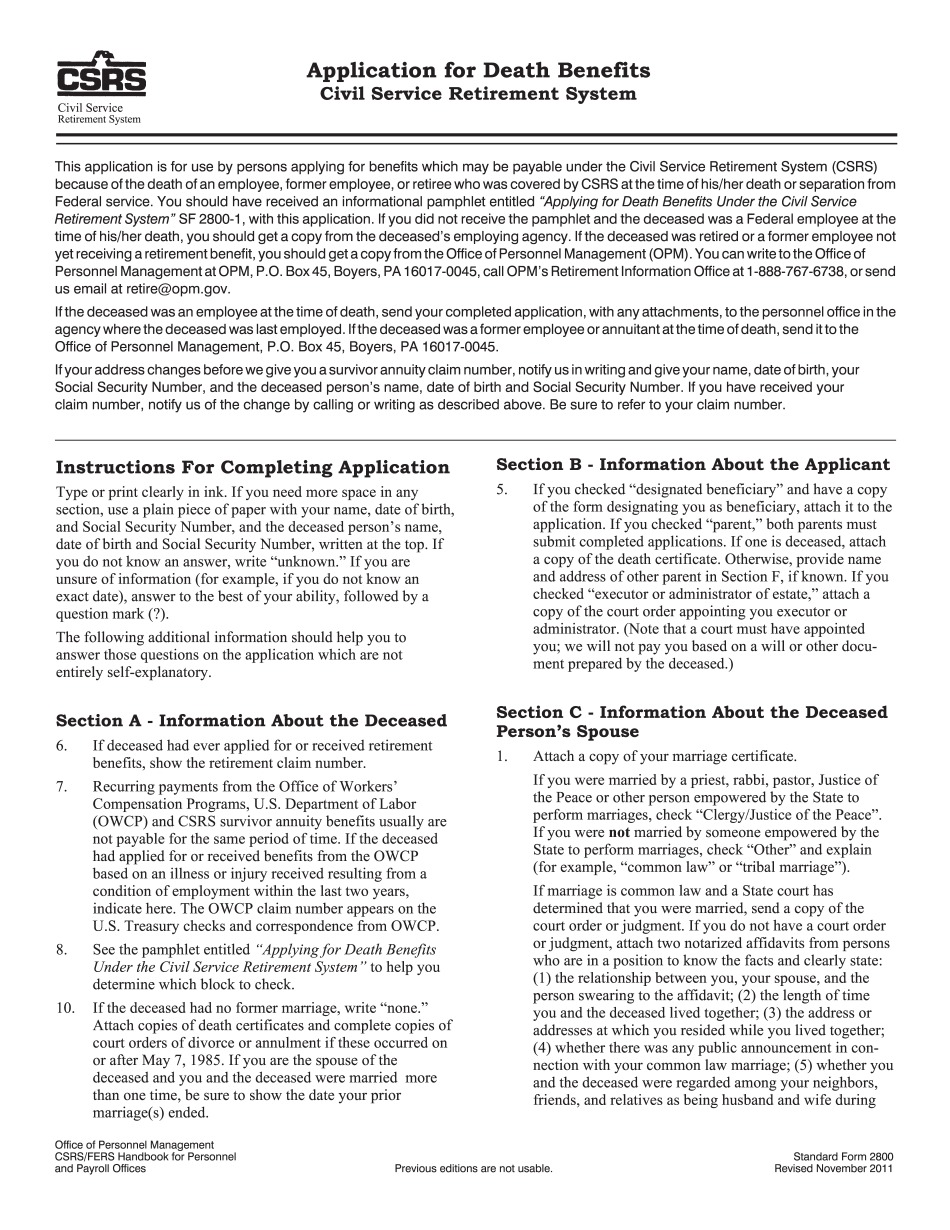

Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits — FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits— FEES — GSA Applying for Death Benefits — FEES — GSA.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Sf 2800, steer clear of blunders along with furnish it in a timely manner:

How to complete any Sf 2800 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Sf 2800 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Sf 2800 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Fers basic employee death benefit 2024